Market Game Theory

Keynes, ever the deep thinker, knew that markets were anything but rational and efficient — as the popular Efficient Market Hypothesis (EMH) now claims. He was too aware of our human nature and particularly the nature of those who drove markets; the people of wealth, the men of industry, and managers of money.

He knew that far from being prudent, these people were prone to irrational exuberance and herd-like behavior. Keynes was the first to codify the truth about the risks of being a contrarian when he said, “worldly wisdom teaches that it is better for [the] reputation to fail conventionally than to succeed unconventionally.”

Since he understood the nature of man, he understood the nature of markets better than most and made a sizable fortune because of it. And there is probably no better analogy on the game of successful market speculation than Keynes’ “Beauty Contest.”

Keynes likened profitable investing to a common newspaper game of the time, “in which the competitors have to pick out the six prettiest faces from 100 photographs, the prize being awarded to the competitor whose choice most nearly corresponds to the average preferences of the competitors as a whole: so that each competitor has to pick, not those faces that he himself finds prettiest, but those he thinks likeliest to catch the fancy of the other competitors, all of whom are looking at the problem from the same point of view… We have reached the third degree where we devote our intelligence to anticipating what the average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth, and higher degrees.”

It doesn’t matter if you’re a value investor or growth focused or a technical trader or you use sun cycles and Fibonacci lines — the goal is all the same. You buy an asset because you think it will go up. And it will only go up if others also at some point, think it will go up. Therefore, to be a successful investor/trader, you need to be good not at identifying what you think are attractive assets, but rather at identifying what other market participants will think is an attractive asset in the future but are underestimating now. And as Keynes said, this is only the “third degree” level of thinking. The real masters are practicing the “fourth, fifth, and higher degrees.”

Fact: In the real world there is no such thing as market equilibrium or intrinsic value. These are PhD constructed mumbo-jumbo. They’re predicated on the grossly asinine assumptions of rational participants and perfect information.

Markets, value, and price are dynamic; meaning they’re ever-changing. They are constantly fluctuating, trending, reverting, and then trending some more; all on the whims of man (and now machine), who’re all playing the “Beauty Contest” game.

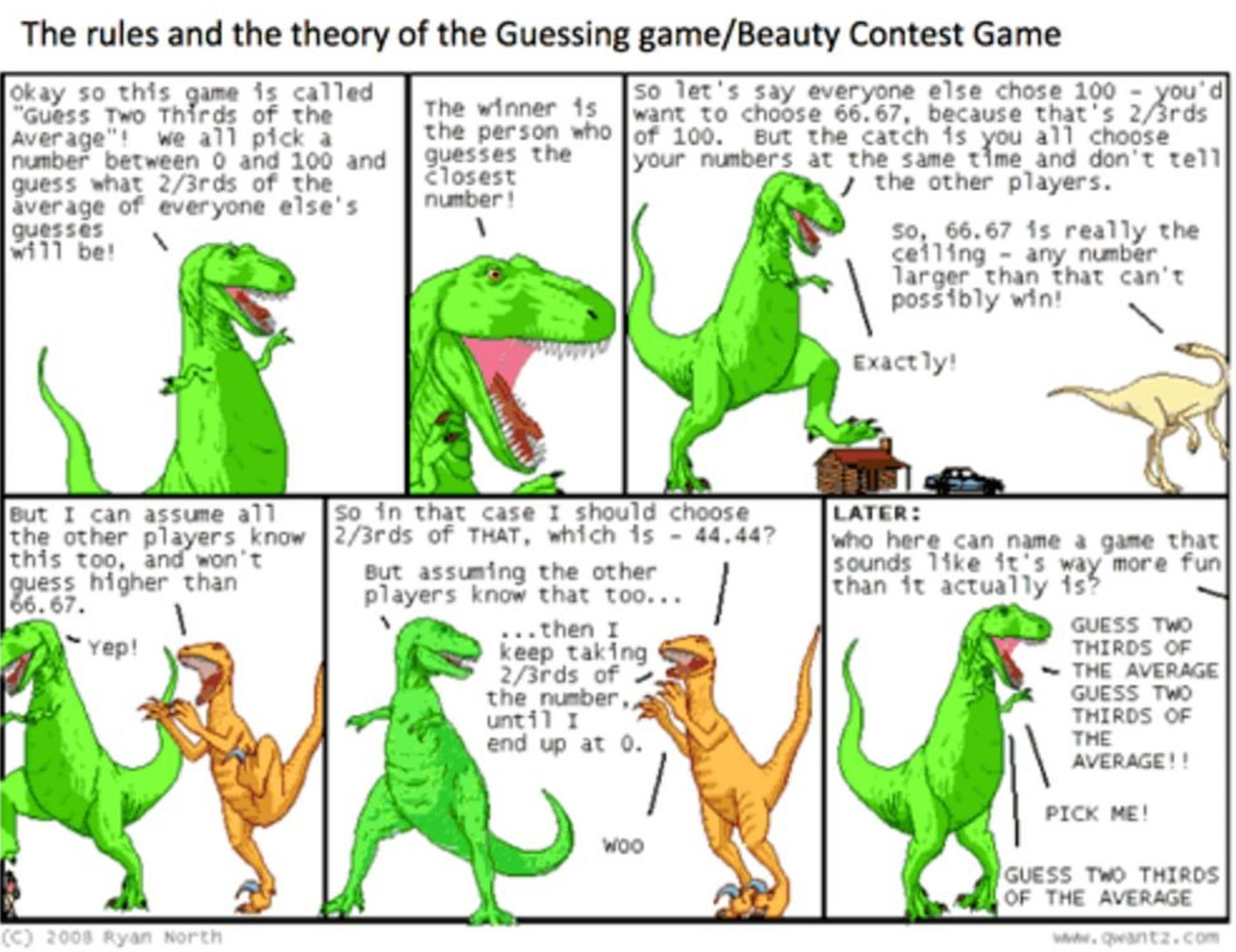

Another way to explore this analogy is to try out this logic puzzle (via FT):

“Guess a number from zero to 100, with the goal of making your guess as close as possible to two-thirds of the average guess of all those participating in the contest. To help you think about this puzzle, suppose there are three players who guessed 20, 30 and 40 respectively. The average guess would be 30, two-thirds of which is 20, so the person who guessed 20 would win.

If you did not enter the contest, you might consider what your guess might have been.

Now that you have thought, consider what I will call a zero-level thinker. He says: “I don’t know. This seems like a math problem. I will just pick a number at random.” Lots of people guessing a number between zero and 100 at random will produce an average guess of 50.

How about a first-level thinker? She says: “The rest of these players don’t like to think much, they will probably pick a number at random, averaging 50, so I should guess 33, two-thirds of 50.”

A second-level thinker will say: “Most players will be first-level thinkers and think that other players are a bit dim, so they will guess 33. Therefore I will guess 22.”

A third-level thinker: “Most players will discern how the game works and will figure that most people will guess 33. As a result they will guess 22, so I will guess 15.”

Where the hell do you get off this train? Well, if you take this higher-level thinking to it’s logical conclusion you get to the Nash equilibrium (named after the mathematician, John Nash, from A Beautiful Mind). The Nash equilibrium is the number that if everyone were to guess it, nobody would want to change their guess. Can you guess?

The answer is zero. Dinosaurs will explain below.

The important thing here is Keynes’ analogy and that markets are dynamic systems predicated on the guessing game played by us irrational humans. And if that doesn’t make ‘em seem complex enough. Just wait, as Billy Mays would say… there’s more! Though Keynes’ beauty contest analogy is great it actually falls short of revealing the true complexity of markets and successful speculation.

Blue pill or red pill?

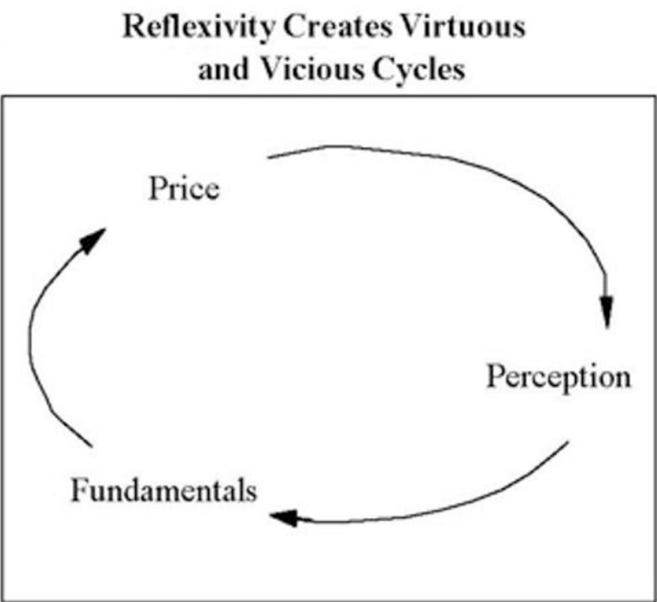

A more apt analogy would not only have participants trying to guess which face would be chosen as the most beautiful, but the beauty contestants’ faces themselves would actually change in attraction based on how participants were voting. Meaning, the contestants’ beauty would be affected by the observers/participants thinking about how others were voting, thus in turn affecting the participants own votes.

What we’re talking about is the “Theory of Reflexivity”, as put forth by Macro legend George Soros (in actuality, the idea was first introduced by sociologist WIlliam Thomas and then brought to Soros’ attention by Karl Popper, his mentor) but Soros was the first to apply it to markets — and with great success, obviously.

Anyways, Wikipedia defines reflexivity as the following:

Reflexivity refers to circular relationships between cause and effect. A reflexive relationship is bidirectional with both the cause and the effect affecting one another in a relationship in which neither can be assigned as causes or effects. In sociology, reflexivity therefore comes to mean an act of self-reference where examination or action "bends back on", refers to, and affects the entity instigating the action or examination.

Reflexivity is centered around the idea of there being two realities; objective realities and subjective realities.

Objective realities are true regardless of what observers/agents think about them. For example, if I remark that it’s snowing outside and it is in fact snowing outside, then that is an objective truth. It would be snowing outside whether I said or thought otherwise — I could say it’s sunny but that would not make it sunny, it would still be snowing.

Subjective realities on the other hand are affected by what the participants think about them. Markets fall into this category.

Since perfect information doesn’t exist (ie, we can’t predict the future and it’s impossible to know all of the variables that are moving markets at any given time) we make our best judgements about what assets (stocks, futures, options etc) should be valued at — we play the beauty contest game.

Our collective thinking is what moves markets and produces winners and losers. Meaning, what we think about reality affects the reality we are thinking about. And the reality we’re thinking about affects our thinking about it.

Take a high-flying tech stock like Amazon (AMZN), for example. The company has made little in the way of income (in relation to its market cap) for the majority of its existence (over 15 years), but the stock has continued to soar because people have formed a number of positive beliefs about the company/stock. These beliefs could be that maybe the company will make tons of money someday because it’s innovative, eating market share, or has a secret profit switch that it can turn on whenever it finally chooses to; or maybe people continue to buy the stock because it’s gone up for a long time and will therefore continue to go up.

In truth, it’s probably many of these reasons and more why investors continue to pile into the stock. The reasons aren’t important, what’s important is that these positive beliefs have directly affected Amazon’s subjective reality.

Here are just a few examples of how Amazon’s fundamentals have been positively affected by investors beliefs:

● The high stock price has allowed the company to receive lower financing costs

● Attract exceptional talent which in turn has led to increased innovation

● Hide costs by including stock options as a large portion of employee compensation

● Unconstrained by the need to produce profits, Amazon has been able to drastically undercut the competition and steal market share

It’s not difficult to imagine another reality in which investors collectively had a more negative or neutral belief about the company/stock throughout its life. Amazon would look very different today. Forced to focus on profits — like most businesses — Amazon perhaps would not have had the explosive sales growth its experienced. Maybe it never would have expanded outside of selling books. Maybe a competitor would have run it out of business.

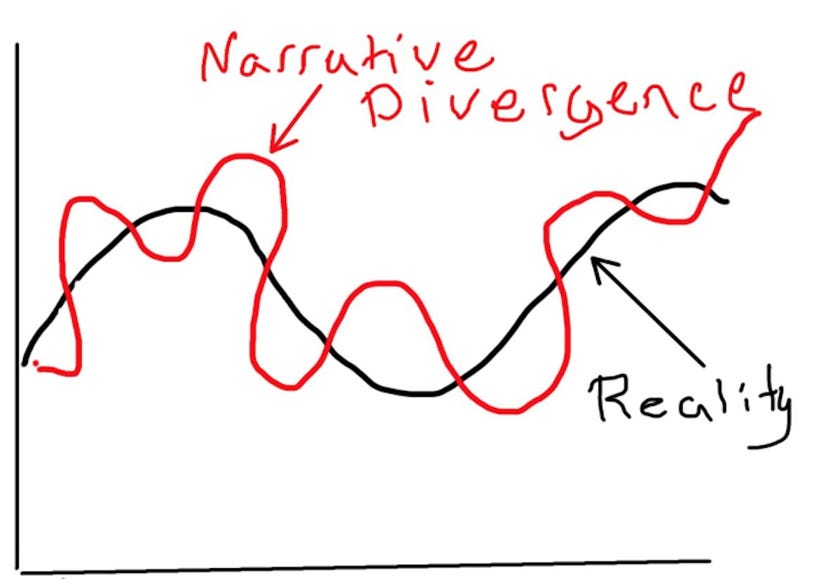

The point is, that markets are reflexive and our beliefs about them directly affect the underlying fundamentals and vice-versa. And sometimes the reflexive mechanism forms a powerful feedback loop and prices and expectations diverge drastically from reality.

Here is Soros on the subject:

Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, a boom-bust process is set in motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced.

What Soros is saying is that markets are in a constant state of divergence from reality — meaning, prices are always wrong. Sometimes this divergence is tiny and imperceptible. Other times this divergence is large, due to feedback loop drivers. These are the boom and bust processes. And it is these large divergences that we as traders want to seek out, because that is where the money is.

There are countless examples of large price/reality divergences in markets. Dutch Tulip-mania in the 17th century, tech bubble of 2000, and the housing bust of 08’ (and nearly every asset in 2016?) are just a few examples of this process at work. Here’s Soros again:

Usually some error in the act of valuation is involved. The most common error is a failure to recognize that a so-called fundamental value is not really independent of the act of valuation. That was the case in the conglomerate boom, where per-share earnings growth could be manufactured by acquisitions, and also in the international lending boom where the lending activities of the banks helped improve the debt ratios that banks used to guide them in their lending activity.

So a lot of what investors consider to be “fundamentals” aren’t really objective facts.

Except…

That’s not completely true either. Because eventually, underlying economics prevail. The narrative divergence between a “false-trend” and reality (real economics) eventually closes. And “fundamentals”, once again become fundamentals — it’s just a function of time. The father of value investing, Benjamin Graham, hit the nail on the head when he said:

In the short run, the market is a voting machine but in the long run, it is a weighing machine.

This means that we can go back and revise our beauty contest analogy one more time. Let’s look at what our final analogy then looks like:

● The key to winning the beauty contest game is not about picking the most beautiful girl. But, about figuring out which girls the average participant thinks the average participant will pick.

● The girls in the beauty contest will become more/less attractive to the voters in relation to how they vote for them. The voters decisions on who to vote for will be affected by the changing attractiveness of the girls.

● Investors operate in dog years (we have short time frames and fall prey to recency bias) and economies operate on, well, much longer time frames. Ugly stocks/assets/markets can be the right pick for a long time in the beauty contest game. But eventually, reality wins out and the dogs are exposed and the lookers get the roses.

Because we don’t just want to win the beauty contest in the short-term, but also in the long run. We have to remain cognizant of when the market has voted the ugly stepsisters as the most beautiful. This is massive narrative/reality divergence. It’s a boom. And all booms are followed by busts.

Sounds difficult right? Well it is. And that’s why successful speculation is so damn hard (and the best game in the world, IMO). There are layers upon layers to this onion. It’s our jobs to keep peeling ‘em back.