- India

- International

Saturday, May 04, 2024

Journalism of Courage

The problems agriculture encountered due to the lockdown had more to do with the demand side. (Express file photo)

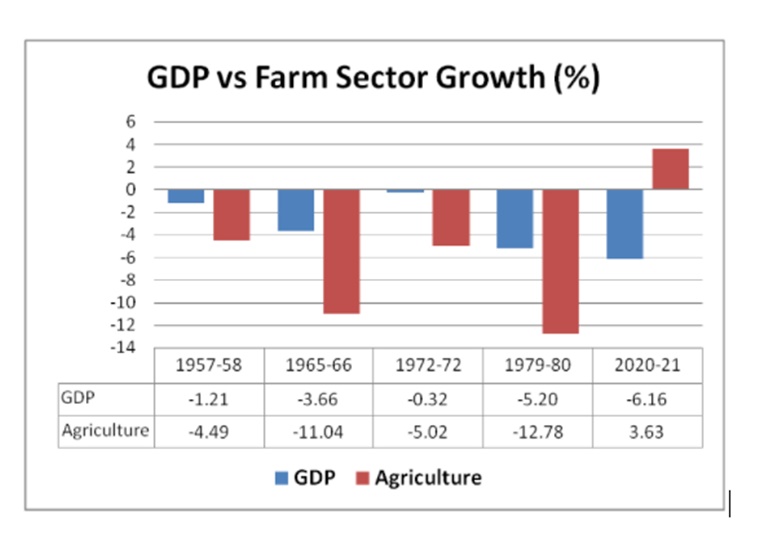

The problems agriculture encountered due to the lockdown had more to do with the demand side. (Express file photo)2020-21 saw the Indian economy register its worst-ever contraction since Independence and also the first since 1979-80. The National Statistical Office has, in its Provisional Estimates released on May 31, pegged the growth in real gross value added at basic prices (previously known as GDP at factor cost) for 2020-21 at minus 6.2%. But what’s unusual this time is that the farm sector (agriculture, forestry & fishing) has grown by 3.6%. As the chart below shows, there have been four instances of negative GDP growth earlier: 1979-80, 1972-73, 1965-66 and 1957-58. All four were drought years, with agricultural de-growth surpassing that of overall GDP in each of them. 2020-21 has been different. There has been record economic contraction, yet no drought; the farm sector actually grew by 3.6%.

Newsletter | Click to get the day’s best explainers in your inbox

Source: National Statistical Office.

Source: National Statistical Office.

There are two main reasons why agriculture didn’t suffer the fate of the rest of the economy last year.

The first is the monsoon.

All-India rainfall during the southwest monsoon season (June-September) was 788.5 mm in 1957, 709.3 mm in 1965, 652.8 mm in 1972, and 707.7 mm in 1979, way below the long period average of 880.6 mm. 2019 and 2020, by contrast, were above-normal monsoon years, with the country receiving an area-weighted rainfall of 971.8 mm and 961.4 mm for the corresponding June-September periods, respectively. The rains were good not just in the main monsoon, but also the post-monsoon (October-December), winter (January-February) and pre-monsoon (March-May) seasons of 2019 and 2020. It led to the filling of reservoirs and recharging of groundwater tables and aquifers, unlike after the deficient monsoons of 2014 and 2015 and the near-deficient one of 2018. Not surprisingly, 2019-20 and 2020-21 produced back-to-back bumper harvests.

The second reason had to do with agriculture being exempted from the nationwide lockdown that followed the first wave of Covid-19.

The Home Ministry’s initial guidelines of May 24-25, 2020 only spared PDS ration shops and other stores selling food, groceries, fruits & vegetables, milk, meat and fish, animal fodder, seeds and pesticides. But within days, on May 27, an addendum was issued, extending the lifting of curbs to fertiliser outlets, all field operations by farmers and farm workers, intra- and inter-state movement of agricultural machinery, sale of produce in wholesale mandis and procurement by government agencies.

The conscious policy call taken to permit agriculture-related activities — and, of course, the inherent resilience and adaptability of rural economic actors — meant that the farm sector was relatively insulated from lockdown-imposed supply-side restrictions. This is clear from all-India retail sales of fertilizers touching 677.02 lakh tonnes (lt) in 2020-21, a sharp jump from the 617.10 lt and 575.69 lt of the preceding two years. It is further corroborated by official sowing data: Total crop acreage in 2020-21 was higher compared to the previous year both during the kharif (from 1,053.52 lakh hectares to 1,113.63 lh) as well as rabi (from 665.59 lh to 684.59 lh) seasons. Simply put, farmers made sure they did not waste a good monsoon, finding ways to even mobilize harvesting and planting labour during peak lockdown.

The problems agriculture encountered due to the lockdown had more to do with the demand side. The closure of hotels, restaurants, roadside eateries, sweetmeat shops, hostels and canteens — and no wedding receptions and other public functions — resulted in a collapse of out-of-home consumption. This was demand destruction not from rising prices — “movement along the demand curve”. Instead, it was from forced consumption reduction, translating into lower demand for farm produce even at the same price — “a leftward shift in the demand curve”.

The Narendra Modi government sought to partly address the demand-side problem through enhanced state crop procurement. The minimum support price (MSP) value of such purchases of wheat, rapeseed-mustard, chana (chickpea), tur (pigeon-pea), paddy and cotton amounted to roughly Rs 130,000 crore during April-July 2020. Together with nearly Rs 21,000 crore of first-installment direct transfers to farmer accounts under the PM-Kisan scheme, it added up to over Rs 1.5 lakh crore of liquidity infusion into the agricultural economy. One must emphasize that MSP procurement was effective largely in crops and regions where the institutions undertaking such operations — be it the Food Corporation of India, NAFED, Cotton Corporation of India or even cooperative dairies — were active and could stem price declines during the period of demand destruction from late-March till July. Such intervention wasn’t possible in non-mainstream produce (vegetables, fruits, poultry, fish, flowers, spices, etc) and regions (maize in Bihar), where the corresponding institutional mechanisms were non-existent.

The demand situation improved, though, with the gradual lifting of lockdown restrictions and also the recovery in global agri-commodity prices. The UN Food and Agricultural Organization’s food price index had plunged to a four-year low in May 2020, following synchronous worldwide lockdowns to contain the spread of the novel coronavirus. But as economies unlocked, prices started rising from around August and the index hit an 83-month-high in April 2021 (see chart below).

Source: Food and Agricultural Organization.

Source: Food and Agricultural Organization.

The benefits of price recovery were really felt during the marketing of the 2020-21 rabi crop, which was a bumper one like that harvested during last year’s lockdown. But this time round, many farmers also realized good prices. The average price of mustard in mandis, according to the official Agmarknet portal, was Rs 5,696.43 per quintal in April 2021, as against Rs 4,492.71 for the same month last year and the government’s MSP of Rs 4,650. It was the same for chana: Rs 5,173.33 versus Rs 4,404.68 and the MSP of Rs 5,100 per quintal. For the first time during the Modi government’s tenure, farmers experienced a Goldilocks moment — of neither drought (like in 2014-15, 2015-16 and 2018-19) nor low prices (2016-17 and 2019-20). Both production and prices were “just right”. Even government wheat and paddy procurement, at 40.5 million tonnes (mt) and 79 mt, respectively so far, has already crossed last year’s all-time-highs.

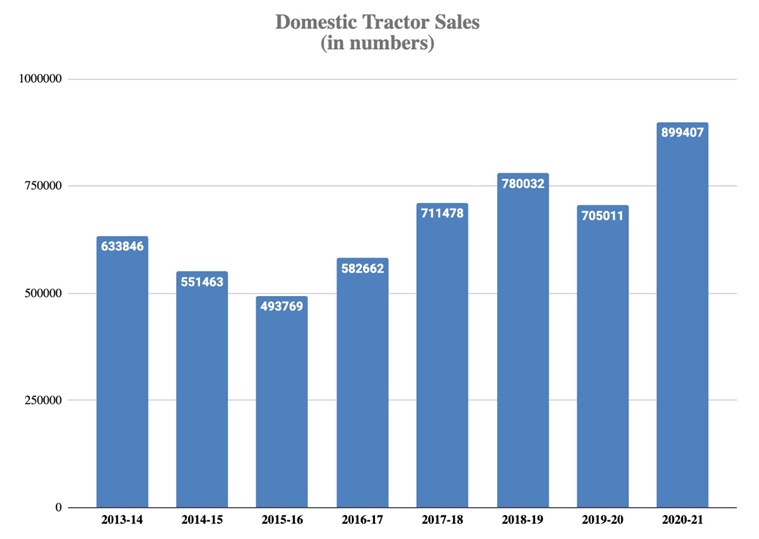

The effects of good monsoon, lockdown exemptions, stepped-up government procurement, and better price realizations were also borne out by domestic tractor sales. At almost 9 lakh units in 2020-21, these, like with fertilizers, were the highest ever for any single year (see chart below). Farm inputs apart, industries such as FMCG and cement, too, seemingly rode high on rural demand.

Source: Tractor and Mechanization Association.

Source: Tractor and Mechanization Association.

While agriculture grew amid an unprecedented economic contraction, 2020-21 was also notable for the record 389.35 crore person-days of employment generated under MGNREGA. With a total spend of Rs 111,207.77 crore, Rs 77,921.25 crore in wages alone, this flagship employment scheme was yet another source of liquidity infusion and, again, a pre-existing programme that the government could deploy to support rural incomes during a crisis. Rural consumption, in turn, provided some cushion to the economy and preventing a bad situation from turning much worse.

The question to ask: Can the above story — of rural playing “saviour” — be repeated in 2021-22?

The one obvious difference between now and last year is Covid-19 cases. Rural areas were mostly unaffected by the pandemic’s first wave. Farm-related activities could, then, go on relatively unhindered, which government policy, whether to do with lockdown or public procurement, also facilitated. That situation has changed with the second wave and rising share of rural districts in total cases, even without factoring in the higher probability of underreporting in these places. Covid’s impact on agriculture per se would depend on the spread, intensity and duration of the infection. Given that the main kharif planting season will take off only after mid-June with the arrival of the monsoon rains, a reduction in the active caseload by then can help avert significant operational disruptions. While fear of the virus may induce precautionary behaviour and postponement of purchases of tractors, two-wheelers or white goods, it is unlikely to affect normal agricultural operations. And if last year’s experience is any guide, the adaptability of farmers and myriad rural economic agents should not be underestimated.

The second factor to be considered is the monsoon. The India Meteorological Department, in its latest June 1 update, has forecast a 74% probability of rainfall during the current season being “normal”, “above-normal” or “excess”. The good news this time is that there is no El Niño — the abnormal warming of the tropical central and eastern Pacific Ocean surface waters, resulting in increased evaporation and cloud-formation activity around South America and away from Asia. The US National Oceanic and Atmospheric Administration has predicted a 67% chance of “neutral” El Niño-Southern Oscillation conditions prevailing through June-August. It has further pointed to increasing chances of a La Niña — El Niño’s counterpart that is associated with above-normal rains and lower temperatures in India — for the autumn and winter months. That augurs well for the next rabi crop too.

It is necessary, however, to note that not every drought or poor-rainfall year (notably 2012 and 2014) has had El Niño, just as 2019 recorded a “strong” El Niño event and yet turned out the wettest-ever year in a quarter of a century. Besides, the monsoon is also influenced by the so-called Indian Ocean Dipole (IOD): A “negative” IOD — wherein the eastern Indian Ocean waters off Indonesia and Australia become unusually warm relative to the western tropical part — is seen as detrimental to rains in India. The IOD is currently “neutral”, but some global models are indicating the possibility of negative conditions developing during the monsoon months. That, along with unseasonal summer showers upsetting the normal heating pattern over the Indian landmass necessary for formation of low-pressure areas (rainfall has been 74% surplus this May), should temper the optimism vis-à-vis El Niño.

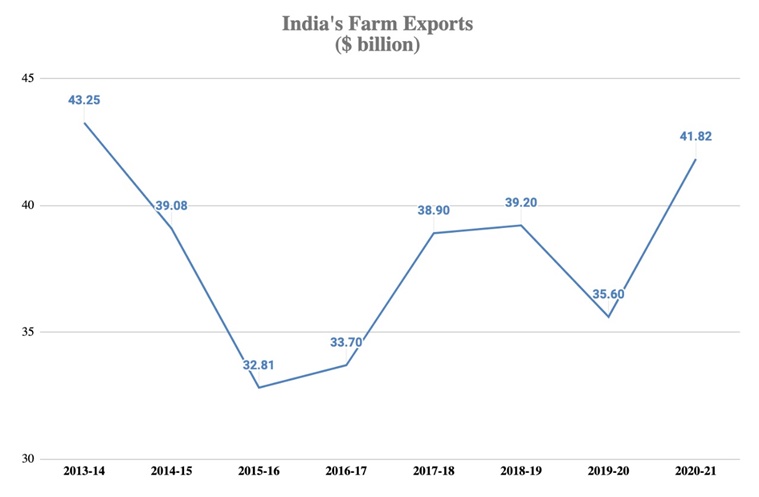

A third source of uncertainty is prices. Global prices — be it of wheat, maize, soyabean, palm oil, sugar, skimmed milk powder or cotton — have scaled multi-year highs in the recent period, helping India’s agri-commodity exports in 2020-21 to recover to near their peak 2013-14 levels (see chart below).

Source: Department of Commerce.

Source: Department of Commerce.

But can export demand alone sustain prices, especially in a scenario where job and income losses, accelerated post the pandemic, have severely dented domestic purchasing power? Moreover, even the benefits reaped by farmers from improved prices in many crops since October-November have been significantly eroded by rising input costs. Diesel prices alone have gone up by over a third in the last one year; so have that of most non-urea fertilizers.

Beyond 2021-22, the real challenge for Indian agriculture and farmers will be on the demand side. That is specifically going to come from declining real incomes and particularly affecting demand for milk, pulses, egg, meat, fruits, vegetables and other protein/micronutrient-rich foods. While rising rural wages and overall incomes is what propelled the demand for these foods in the past — in turn, contributing to dietary and cropping diversification — the ongoing slide presents a frightening proposition. This is a topic deserving separate analysis.

(Damodaran is National Rural Affairs & Agriculture Editor of The Indian Express and Krishnamurthy is Associate Professor of Sociology and Anthropology at Ashoka University. Both are Seniors Fellows at the Centre for Policy Research)

It is imperative we teach our kids how to behaveSubscriber Only

How DDA built the middle class dream and shaped modernSubscriber Only

16th edition of the Habitat Film Festival to begin inSubscriber Only

India's dark chocolate market is growing. Who is taking theSubscriber Only

The complex journey of transgender rights in ChristianitySubscriber Only