Mural Fintech

The Global Buy Now Pay Later Boom

A look at what the future might hold for BNPL

By Henry O’Brien and Charles Lucas for Mural

So the saying goes, “history doesn’t repeat itself, but it often rhymes”

Buy Now Pay Later is booming and so is interest in the space. We take an updated look at this “boom”. Perhaps we may even be found guilty of adding fuel to the fire, as we discuss its future by examining its past.

As we dig into the origins of BNPL and take a look at Private Label Credit Cards, we can’t help but think they must be gasping with disbelief. But the genius of BNPL is that it has borrowed old ideas about credit, walked the paths trodden by pioneers such as PayPal, and added technology and some ideas of its own to create a new product that consumers and merchants love; particularly the newly minted mega consumers (GenZ).

How did BNPL reinvent point of sale finance, lend vast sums all over the world, be almost completely unregulated and in some cases, become bigger brands than the brands they are working to support? And what might happen next?

History is more or less bunk — Henry Ford

There’s nothing new about point-of-sale credit. After all, Madame Bovary (Gustave Flaubert, published 1856) falls into debt with the local haberdasher in Yonville who sells her stock on credit to boost his sales. Bovary’s downfall becomes certain when she is unable to repay him and he sells her debts to a banker in nearby Rouen. And credit at the checkout didn’t start in the nineteenth century; shops have probably been boosting sales by giving credit to customers since at least Phoenician times.

For many years, retailers, credit card issuers, and consumer finance companies have been changing and tinkering with the ways of offering credit at the point-of-sale (POS). They have had to juggle the countervailing forces of the consumers’ demand for more or less instant and frictionless checkout and the need to do credit checks and prevent fraud.

Globally, BNPL’s growth has been staggering. A study by Kaleido Intelligence estimates that the global market will grow from $89 billion in 2020 to $352 billion by 2025, a growth rate of almost 400%. They also reckon that by 2025 $731 billion will be spent globally using digital point of sale financing options, largely BNPL.

But while BNPL is growing fast, it is still dwarfed by credit card borrowings. For this, where else to look but the US, where credit card balances are approaching $1 trillion. However, growth among traditional credit card issuers has been slowing, and in some cases shrinking. The US’s largest credit card issuer, JP Morgan Chase has kept its receivables flat Y/Y at around $142 billion (2Q21 vs. 2Q20), whilst the next largest issuer Citibank, with $125 billion of card receivables, has seen balances decline by 3%, and Capital One, with $99 billion of the nation’s domestic credit card debt, has seen its balances shrink by 4% since the summer of 2020. Whilst the US’s debt service burden is hovering around generational lows, it’s a wonder where newly originated consumer credit is ending up.

Among the many reasons for this stagnation, two stand out. Changing consumer habits — GenZ consumers are more wary of getting into debt than their baby boomer parents and the rise of BNPL. BNPL has been dubbed by some as “the future of millennial finance”, while others see a consumer finance craze that, just like most others will go phut! sooner or later. Some see it as a moral response to usurious consumer lending and others see a regulatory car crash happening in front of our eyes.

PayPal the pioneer

PayPal was founded in 1998 (then called Confinity) and shortly after listing in 2002 was acquired by eBay for $1.5 billion. From the start it was a blow out success. Within a short space of time, more than 70% of all eBay auctions accepted PayPal payments and roughly 1 in 4 completed auctions were transacted via PayPal.

Like many great innovators, PayPal’s aim was simple and bold: create trust between strangers transacting online. For shoppers it meant protection from being sold counterfeit products or being sold things that never arrived. For merchants, it meant getting paid when they kept their side of the bargain and delivered the goods. For this PayPal charged a fee.

PayPal established the value of owning the customer early on, and it wasn’t long until they also established the importance of owning the merchant relationship. And in finding a role to play as a valuable intermediary, they built what can be considered the first mass adopted digital wallet. As they built a tremendous moat around their business, they also managed to upset some of the most notable payments players!

By owning the network and controlling the merchant relationship, PayPal was able to negotiate healthy fees for themselves (as opposed to being told what they would receive from the networks). It’s therefore no surprise to see the most established BNPL providers adopting a similar closed loop strategy. Perhaps it’s no coincidence that the US’s largest BNPL provider Affirm was established by PayPal’s very own Max Levchin.

After a while (and inevitably) credit was added to the PayPal offering. In late 2008, eBay, PayPal’s parent, acquired Bill Me Later for $945 million (10x TTM / 6x forecasted NTM revenues) which later became PayPal Credit and today, houses their BNPL division. Bill Me Later had been through many changes pre-PayPal, but ultimately found its place in the market — performing instant credit checks on internet users so that they could buy goods online without using a credit card. Déjà vu.

Meanwhile in Sweden

Meanwhile in Sweden, Klarna was figuring out how to help merchants sell more by building trust and increasing convenience for shoppers who favoured debit cards over credit cards, but didn’t like to use them online. It took a surprisingly long time before they added credit at the checkout.

Some ten years after it started in 2005, Klarna’s model remained simple: buy now, pay upon receipt. This included an option to return items without any money ever leaving the customer’s account. Klarna simply (and effectively) de-risked the online shopping experience by taking the risk that the customer would not pay and promised that merchants they would see an increase in sales. In return, Klarna charged the merchant a “PayPal like” fee. Klarna’s variable fees can still reach as high as 5.99% in the US for an interest free 30 day full line of credit.

It was in 2017 that Klarna took the leap to becoming a real fintech and became a bank. Arguably borrowing ideas from from the private label credit cards, it started offering interest free instalment credit at the checkout. It turned out that smoothing down the rough edges of the checkout experience was nice, but giving more or less instant interest free credit really made the difference and caused volumes to really skyrocket.

The USP of BNPL (according to Klarna)

Klarna isn’t shy about stating the benefits they claim BNPL offers merchants:

- The merchant isn’t at risk of not getting paid. Klarna pays the merchant and in turn collects from customers

- Retailers typically see a 68% increase in average order value with a Klarna button at the checkout

- 58% boost in average order value for retailers offering Klarna Financing

- 20% increase in purchase frequency for customers shopping with Klarna Pay in 30 days

- 44% of users say they would have abandoned their purchase if Pay later wasn’t available

A look at private label credit cards

As suggested above, we think there are many similarities between the BNPL providers of today and the long established Private Label Credit Card (PLCC) industry. But first a quick definition: a private label credit card (or store card) is a card issued by a credit provider on behalf of a merchant. The card can only be used for purchases at that specific merchant.

PLCCs shouldn’t be confused with co-branded credit cards such as the Mastercard issued Amazon credit card which can be used anywhere, but where spending at Amazon yields additional bonuses, points or discounts (another good example would be the popular British Airways branded American Express card).

Unsurprisingly, PLCCs are in their element in the United States, where they are big business. Outstanding balances held on PLCCs in the US stood around $200 billion as of 2020 (vs. BNPL lending estimated at $40 billion).

Why is this relevant to BNPL?

PLCC providers have long boasted of the benefits that their stores get from issuing their cards — increased loyalty, better data and hence better data driven marketing, higher spend per sale, and more sales. Sound familiar?

To dig into one major differentiator — the data. With a Visa issued card for example (the four-party model), the lender knows only how much was spent and where, whereas a PLCC issuer knows exactly what was bought — the advantage of obtaining SKU level data. In this data driven world it’s obvious why this matters and what can be done with such detailed information. We must also note, because PLCCs can be used only at the issuing merchant, there are important operating cost reductions — no interchange or scheme fees. This “closed-loop network” is also an important part of the equation for BNPL providers.

So back to BNPL

Enough history and precedent! When you think about the PLCC industry, BNPL starts to look very similar, albeit slightly more advanced and with an undoubtedly brighter future.

There are various opinions as to what BNPL really is. Is it a payments mechanism or is it a point of sale lender (credit)? Its history of taking away the inconvenience and lack of trust when shopping on-line suggests that it is a payments mechanism, albeit an innovative one. Klarna also offers merchants “a complete checkout solution”. But it was the addition of credit that evidently caused volumes and its popularity to take off and it was credit that, to our way of thinking, changed BNPL profoundly. Today, it is credit that truly underpins economic returns for these companies and it will likely be issues tied to credit that determine its future. It’s perhaps no surprise then, that we view BNPL providers to be more credit than payments. And we think regulators see it the same way.

How do BNPL platforms make money if customers don’t pay interest? And what about the credit risk? Simple, the merchant pays a commission to the BNPL provider on the price of the goods financed. If the BNPL provider receives 3% from the merchant and the consumer repays the amount in three equal, monthly instalments, one of which is immediate, that is equivalent to an annual rate of around 45% (IRR). Charging merchants 5.99% to offer the shopper 30 days “interest free” credit (plus transactions fees) throws off an IRR of more than 112%. Albeit for illustrative purposes, as this doesn’t take into account gateway and/or acquiring fees that erode the gross transaction margin, but we’ll dig into that another time.

Merchants also pay monthly fees and setup costs. From then on BNPL is a straightforward net interest margin business familiar to bankers all over the world. From the 45%, the provider must pay for its funding (for example, Klarna is a bank and takes deposits on the web), bad debts, operating and marketing costs.

Obviously in financials services, there is more. The borrower/consumer must pay interest and late fees if repayments are not made on time (around 19% for Klarna). With UK regulators closing in on the space, Klarna have recently done away with late fees, although we find it difficult to imagine a world where credit is extended to consumers without repercussions for defaulting.

Increasingly BNPL providers are also providing interest bearing loans to consumers. In its most recent earnings (F4Q21), US market leader Affirm disclosed that 62% of gross merchandise volume (GMV) in the quarter was interest bearing (vs. 38% at 0% APR). Described this way, BNPL seems a pretty conventional spread banking business. But a few things do make it different:

- Providing zero percent interest loans repaid in three or four monthly instalments available at a website’s checkout was/is an exciting innovation. Customers love it. Some have said they’ll leave a site if they’re not able to pay with their preferred BNPL provider;

- Lending decisions are extremely fast and easy for the customer. BNPL is all about removing friction around spending and smoothing the checkout experience for consumers;

- Zero interest credit is extremely appealing when compared with the roughly 30% offered by credit card lenders. Many GenZ consumers don’t even have credit cards.

What’s fair?

Klarna makes a moral or fairness argument. It argues that consumers are being ripped off by the high interest rates charged by credit card lenders and its zero cost loans are far better value and furthermore they are more transparent about the charges that they do levy (e.g. late fees and interest).

Another recent UK campaign cited that “Brits paid £5.7 billion in credit card interest and fees in 2020!” #whypayinterest

These are fair points, for sure. Their critics argue that the moral argument is not so straightforward. They say that the astonishing ease with which consumers can obtain credit is part of the problem and it tends to load unnecessary debt on to consumers. The reason that retailers love BNPL (it boosts sales) is the very reason that consumers should be wary of it as these increased sales arise (partly) as a result of increased consumer debt.

Furthermore the moment that a consumer decides to borrow, is the moment they are looking at the items they want to buy: hardly the moment of greatest rationality and measured decision making! All fair points too.

Perhaps made all the fairer by surveys that show that many BNPL users don’t realise that they are borrowing.

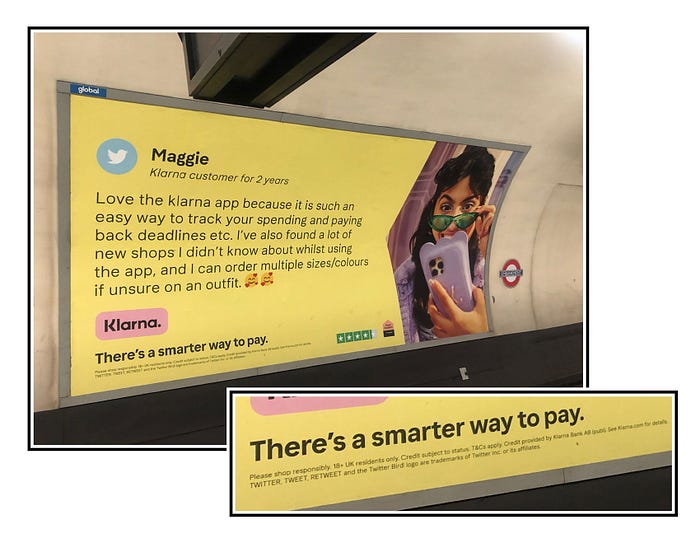

This picture of a Klarna ad on the London Underground tells us a number of things about the industry. And it’s likely that the small print at the bottom will catch any regulator’s eye even if you can’t quite read it from the platform — ‘Please shop responsibly’. Warnings like this are more common on gambling sites. If that doesn’t point the way to future regulation, what does?

Regulation is coming

BNPL is a global phenomenon but to keep it short (ish) we look at the UK for they are arguably making the most noise at the time of writing. In February 2021 the UK’s Financial Conduct Authority (FCA) published the Woolard Review- A review of change and innovation in the unsecured credit market.

Unsurprisingly it had a lot to say about BNPL. The first thing was that BNPL falls outside the scope of regulation and so unlike most consumer credit, BNPL is completely unregulated. The government announced that it would legislate to bring BNPL under FCA’s regulation. We can only speculate what the regulation will look like but it seems probable that BNPL lenders will have to do significantly more credit checks and (crucially) affordability checks before approving the advance.

An October 2021 update from the UK Government can be found here.

We might also add that UK nonprofit Citizens Advice research found that one in ten BNPL shoppers had been chased by debt collectors, with numbers closer to one in eight for younger people. The charity also cited findings that BNPL shoppers in the UK were charged £39 million in late fees in the twelve months prior to September 2021. And with outstanding loan balances recently surpassing £4 billion, it is also no surprise that Britain’s biggest consumer group recently urged its government to fast-track regulation.

Given that BNPL exists in order to smooth and enhance the checkout experience to boost sales, introducing ‘clunky’ credit and affordability checks, form filling and such like may rob BNPL of some of its potency.

Competition is already fierce

No one can doubt that there’s plenty of competition between payment methods and credit at the checkout. But there is only so much real estate to be allocated to BNPL providers. Here‘s a snapshot from our favourite fast fashion website Pretty Little Thing:

dealroom.io shows that over a hundred consumer facing BNPL providers have raised over $8 billion of growth capital, but when it comes to visibility, it’s tough to see room for more than a handful. And that’s not to mention offerings from PSPs, challenger banks, B2B, super apps or vertically specialised BNPL providers. That’s a lot of ways to pay and and a lot of ways to borrow!

Banks are also seeking to join the BNPL party. For example, neobank Monzo gives its customers a BNPL loan and as Monzo has no connection with the merchant it’s unlikely to get the full fee benefits that can be achieved by those who are both the issuer and the acquirer i.e. Klarna or similar. And what’s more, they won’t get the same level of data. To us, it’s hard to see how this will solve their issues around turning a profit and looks like more of a customer engagement and acquisition tool than a money maker. But it’s notable nonetheless and highlights how increasingly crowded the space is getting. And Monzo are not alone, Revolut is doing something similar. So are Citibank, Chase, Tinkoff, Marcus, Curve, Upgrade…

These facilities are being supported by the networks, as they find themselves being cut out of the transaction when pure play BNPL providers come to play.

The news flow around BNPL is tough to keep up with, but here are some recent and notable events:

- Square triggered a slew of BNPL related events with their $29 billion acquisition of Australia’s Afterpay;

- Mastercard has announced “Mastercard Installments” to “make it easy for any lender to provide a BNPL product by using the Mastercard payment rails” ;

- Visa is right there alongside them, launching “Visa Installments” with FIS, Moneris, Global Payments, ANZ, CIBC, HSBC, ScotiaBank, among others already adopting it;

- Amex have recently launched their own “Plan It” offering;

- PayPal removed late fees globally

- And then announced the acquisition of Japan’s largest BNPL provider, Paidy

- Amazon announced its partnership with Affirm to deliver “Pay-Over-Time” option at checkout (when Amazon moves in on something, watch out)

So how will BNPL develop and what should you look out for?

Predictions are for the brave (or for the mugs) but this is what we think will be significant in the coming months and years.

- High Growth: BNPL will continue to grow quickly. Both consumers and merchants love it.

- But margins will decline: the level of competition is very high both in terms of the number of players and the specification of the product (for example PayPal and Klarna no longer charge late fees). We think it is inevitable that providers will compete on price and margins will be squeezed.

- Regulation: will become a big issue and complying with it will go to the heart of what BNPL is all about: creating a frictionless checkout experience and boosting sales using credit. If regulation gets in the way of experience, this could prove to be an existential threat. Don’t underestimate the regulator. Klarna for one, has quickly moved ahead of regulations being introduced removing late fees and strengthening credit checks

Once upon a time the payday lenders argued that they were providing a useful social service and that regulators agreed with them. Perhaps they did agree for a time but regulation then forced them out of business. No one is suggesting that BNPL is the same as payday lending. The point is that regulation is a force to be reckoned with.

- Scale will prove super important: The twin forces of competition (margin pressure) and regulation will give the large BNPL providers a significant advantage over the smaller players. Not just because with scale comes operating efficiencies but more structural advantages too. For example, if regulation makes customer take-on more cumbersome and the checkout experience becomes clunky (see point above), the large providers will have a huge advantage over the small ones because they will have a large ‘stock’ of pre-approved borrowers for whom checking out using their BNPL product will be quick and easy. Naturally merchants will prefer these large providers and the large providers with more merchants will be preferred by consumers and so the virtuous circle will turn.

- BNPL itself will become less important: More credit provided at checkout will be interest bearing. If instant credit approval (one of the features of BNPL today) is no longer quite so instant owing to regulation or other factors, we think that consumers will be guided towards interest bearing credit (probably for the larger items).

- Brand not credit: BNPL providers will increasingly compete by being brands in their own right and consumers will use them not only at checkout but will use them to find the retailers in the first place. A play with Klarna’s app and website shows that Klarna is already well down this road. The Klarna ad on the Underground shown above has the telling phrase ‘… I’ve also found a lot of new shops I didn’t know about whilst using the app…’

- Will BNPL kill the credit card? We don’t think it’s as simple as that. What do we mean when we say credit card? Do you mean the lender (issuer) or do you mean the Visa or Mastercard network? The lenders will compete on price with the BNPL providers and there’s nothing new about price competition in financial services. It seems unlikely that this competition will be to the death. The network payment rails are extensive and efficient movers of vast sums of money around the world. That is not profoundly threatened by an emerging form of credit. Put another way, what fraction of your spending do you imagine doing via BNPL? The rest you’re likely to do with the physical or virtual card in your wallet. You probably won’t be using BNPL as you click on to public transport or as you checkout at the supermarket or hairdresser.

But we could see a full revolution of the innovation cycle. As discussed in Scale will prove super important… above, a large BNPL provider will have a large stock of pre-approved borrowers with credit limits in place. It feels like it will be only a short step to make this credit available not just at the checkout but via a card. A Klarna credit card, why not?

- Retailers and BNPL providers may become hard to distinguish: Klarna’s app is already starting to look like a storefront and when Amazon’s partnership with Affirm is set up, will the consumer know or care if Amazon or Affirm is providing the credit that makes their life so easy at checkout? When we talk about embedded finance, this is just what we mean.

- Lending is lending: the old fashioned skills of credit control and balance sheet and liquidity management will be as crucial as ever. At the heart of BNPL lies a lending and spread business and no amount of clever tech will change that.

If we are to draw to one conclusion, it is this. BNPL will become less of “a stand alone thing”. It will become increasingly embedded in the merchant’s platform and ultimately become ultimately less visible. This will be driven by the economics of BNPL and a closer look at those numbers will be the subject of our next piece on the space.