A Brief History of the World (of Venture Capital)

The Family Papers #019

By (Co-Founder & Director) |

Venture capital is so familiar in the startup world that everybody tends to forget how it emerged and why it is so focused on financing startups. The reason why venture capital thrives in the digital economy has been discussed in a previous issue. Its history, on the other hand, is not well known. Much has been written on the subject, notably by Carlota Perez, William Janeway, and Steve Blank. Here is a brief version.

Before Equity Came to Be

For most of capitalism’s history, entrepreneurial ventures were financed through credit instead of equity. There are several reasons why it was preferable for financiers to lend money to companies rather than to buy shares in them.

First, available information systems were not very effective in tracking what happened in a company’s operations and finances. Retail businesses had to wait for the cash register (invented in 1879 in Dayton, Ohio) to entrust their employees with the company’s day-to-day money. So we can imagine what it meant for shareholders to trust an entire company with the much higher sums they were willing to invest. How could they make sure the money was put to work in the company and not embezzled by the CEO or their employees? Without a proper information system it was difficult to determine how much profit a company made, let alone if it made a profit at all. The easier way to secure a return on one’s investment was to lend money and submit a claim for reimbursement at the agreed date, whatever the situation of the company. (In the old days, shareholders’ liability was mostly unlimited, so even if the company didn’t exist anymore, the debt could be recovered from its shareholders.)

By the way, that unlimited liability was another reason why credit was long favored over equity. Before limited liability became common practice, if you owned a company’s shares you were potentially liable for all the money that company owed other stakeholders. As a result, it was very risky to take an equity stake in a company: you had to know the entrepreneur, live nearby to keep an eye on them, and make sure that they didn’t make any decisions that could result in somebody taking your wealth away from you.

This all changed when limited liability became the norm for corporations—a brand new world that was created in 1811 in the state of New York. As written by The Economist in a 1999 article, “in 1811 New York state brought in a general limited-liability law for manufacturing companies. Its popularity, and the flight of capital to states with limited liability from those without, led most American states to follow suit. In 1854, Britain, the world’s leading economic power, did so too.” (As of today, the fact that New York City remains the financial capital of the world is a testament to that legacy: they were first, and they’re still on top.)

Before those two things existed — reliable information systems and shareholders’ limited liability — lending money was much safer than buying shares. Indeed investing in equity remained marginal, except for the occasional exuberance that contributed to discredit it even more, as explained in The Economist:

Shares were first issued in the 16th century, by Europe’s new joint-stock companies, led by the Muscovy Company, set up in London in 1553 to trade with Russia. (Bonds, from the French government, made their debut in 1555.) Equity’s popularity waxed and waned over the next 300 years or so, soaring with the South Sea and Mississippi bubbles, then slumping, after both burst in 1720. But share-owning was mainly a gamble for the wealthy few, though by the early 19th century in London, Amsterdam and New York trading had moved from the coffee houses into specialised exchanges.

Only in some cases did investments usually take the form of equity. Maritime expeditions were one case. They could even be considered the primitive form of venture capitalism. Just as navigators were the most adventurous entrepreneurs of their time, shipowners were the first venture capitalists in economic history. The reason why they could do so is because the maritime industry had its own, specific ways of dealing with the absence of both information systems and limited liability.

If a vessel went to sea, there were three possible outcomes. The ship could sink: in that case, everything was lost. Insurance was eventually invented, thousands of years ago, to cover that risk. The ship could also come back after having reached its initial destination, in which case it was easy to count the merchandise and share the profit. A ship, after all, is a reliable information system: your assets are all that is on board, and the sailors can testify that the captain didn’t divert part of the cargo. The third outcome was that the ship was attacked by pirates or, worse, embezzled by its own crew. In that case, investigations could help the shipowner find the culprits, who were then put in prison, tried and executed—a fate frightening enough to dissuade entrepreneurs from walking off with shareholders’ cargo.

By the way, ship owners and ship captains invented the carried interest, as related by Morris Peal, of the group Patriotic Millionaires:

The term originated from the practice of ship owners and ship captains getting a 20 percent commission on the things they carried. If you were going to operate a ship and drive it from, say, the New World back to Europe with some valuable cargo, you and the captain of the ship would keep an interest of 20 percent for whatever you carried. So it’s called the carried interest.

Learning to Invest in Equity

Even in the presence of reliable information systems and limited liability, buying stocks in new ventures long remained a privilege for the wealthy. It was difficult for Entrepreneurs to advertise their new ventures on the marketplace, and the public preferred to own shares in existing, listed companies anyway.

But there were exceptions. The Railway Mania that took place in Britain in the 1840s saw the public buy shares hand over fist in newly founded railroad companies. The reason why these were relatively more attractive was that the money was allocated to financing tangible assets: if the company failed (and a lot of them did), it was supposedly still possible to seize the assets and sell them on the market to partially recoup the initial investment. In any case, the presence of tangible assets made it easier to value the companies and to put a price on the shares.

Later, at the beginning of the 20th century, Henry Goldman (the son of the ‘Goldman’ in Goldman Sachs) found a way to underwrite securities for a new breed of companies that didn’t own tangible assets of substantial value: retailers and manufacturers of consumer goods. As recounted by Charles D. Ellis in The Partnership: The Making of Goldman Sachs,

The public securities markets, both debt and equity, had always been carefully based on the balance sheets and the capital assets of the corporations being financed—which is why railroads were such important clients. To expand, United Cigar needed long-term capital. Its business economics were like a “mercantile” or trading organization’s—good earnings, but little in capital assets. In discussions with United’s half dozen shareholders, Henry Goldman showed his creativity in finance: he developed the pathbreaking concept that mercantile companies, such as wholesalers and retailers—having meager assets to serve as collateral for mortgage loans, the traditional foundation for any public financing of corporations—deserved and could obtain a market value for their business franchise with consumers: their earning power.

Consequently, the first half of the 20th century saw investment opportunities extended to two categories of ventures: those that deployed valuable tangible assets (railroads, later telcos) and those that operated a retail business (such as Goldman Sachs’s client United Cigar). Before World War II, banks and the public would buy shares in or lend money to companies with tangible assets or a recurring revenue derived from a retailing business.

The problem is that technology-focused entrepreneurial ventures didn’t fall into either category. They couldn’t borrow from banks because their business model was unknown and they still had everything to prove. And they couldn’t raise capital from the public because no financier could value them. This gap led to the emergence of private equity: because it was so risky, technology ventures were forced to rely on wealthy individuals. In some cases those were syndicated by a merchant banker, who co-invested with his clients. But those deals usually failed to generate enough money to finance very ambitious ventures—except if they were carried out by exceptional financiers such as Lazard’s André Meyer or Warburg Pincus’ Lionel Pincus.

This is why the government initially played a key role in financing technology companies, especially following World War II.

The Government’s Critical Role

The detailed story of how the US government contributed a great deal to financing technology has been told by many authors, notably in his unique and absorbing Secret History of Silicon Valley.

When the Japanese attacked the United States at Pearl Harbor, it was a wake-up call. Suddenly, the US found itself at war with Japan in the Pacific and Germany in Europe. Both Axis nations were powered by impressive scientific and technological capabilities. Germany, notably, had a superior academic apparatus, with all those Nobel Prizes in physics and chemistry, that helped its army deploy advanced radar technologies designed to help bring down US bombers — to the point where the probability of an American bomber pilot surviving the war in Europe was no higher than 25%.

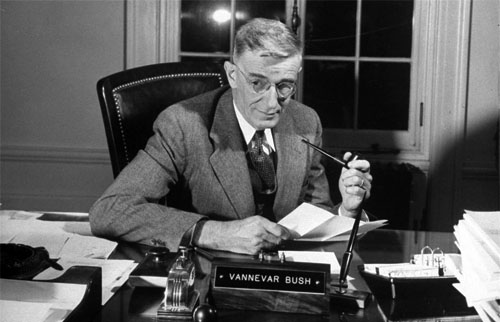

This challenge was tackled by the Roosevelt administration with the help of a renowned engineering scholar named Vannevar Bush, who went on to chair the newly formed Office of Scientific Research and Development (OSRD).

The problem that Bush was trying to solve was that the military needed top-notch researchers, but the best researchers preferred to join academia than enroll in the military. As a result, only a few scientists accepted being placed in charge of in-house military research, and those that did were clearly not the best. Bush, who previously worked in the MIT Department of Electrical Engineering, persuaded President Roosevelt to give up on enrolling researchers in the military in favor of allocating public funds to the best universities in the country. Instead of recruiting researchers and forcing them to renounce their academic careers in the process, why not leave them where they are and provide them with the resources necessary to conduct their research on matters that were of interest to the US military?

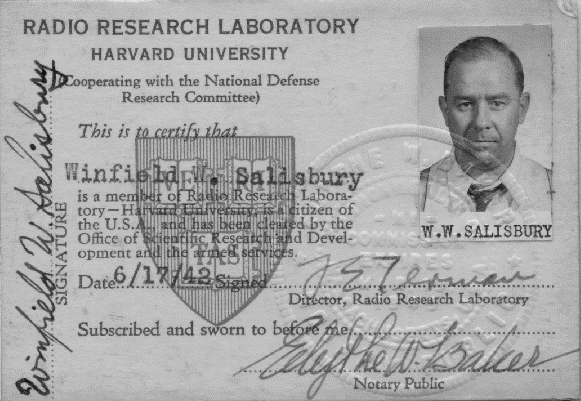

A lot of money was subsequently poured into elite universities, all of them located on the East Coast. At Harvard University and MIT in Cambridge, and at Columbia University in New York City, secret research laboratories were inundated with public money and crowded with the best scientists in the country, all with one mission: to invent the new, cutting-edge technologies that would help the US regain the upper hand. Among those secret laboratories was the Radio Research Laboratory at Harvard University (where research aimed at finding ways to block enemy radar), whose head was Frederick Terman, a member of Stanford University’s engineering faculty and one of Vannevar Bush’s former MIT students.

After the end of World War II, again following Vannevar Bush’s recommendations, a massive amount of public spending was once again allocated to continuing the research effort. The war, after all, wasn’t really over: there was the Korean war, then the Cold War. The G.I. Bill, designed to encourage veterans to attend university so as to facilitate their return and help them find jobs, matched the effort on the research front with a massive upheaval of the country’s higher education system. Both efforts, in research and in higher education, contributed to turning the US academic system into a powerful growth-generating machine, which in turn triggered the post-war boom. (In many ways, we’re still trapped in an idea inspired by that specific period: that our prosperity depends primarily on universities—when in fact, in the current period, it depends more on entrepreneurship.)

In that context, a new challenge was to convert the US industry from manufacturing weapon systems to manufacturing consumer goods. A few wealthy families created their own investment firms to seize the opportunities brought about by the end of the wartime economy. The Whitneys founded J.H. Whitney & Co., the Rockefellers founded Rockefeller Brothers, Inc. (later Venrock) and the Phippses founded Bessemer Securities. All those took investing in technology companies to the next level. For instance, J.H. Whitney purchased Spencer Chemicals to convert a munitions plant into a fertilizer facility. With those new family-funded firms, private equity became more professional. Instead of acting as co-investors as did the old-fashioned merchant bankers, professional management teams took charge of sourcing opportunities, evaluating risks, and negotiating investment deals on behalf of their shareholders.

Laying the Ground for Venture Capital

The first self-proclaimed venture capital firm was the American Research & Development Corporation (ARD), founded in 1946 by the famous Harvard Business School professor Georges Doriot—an emigrated Frenchman who became a general in the US military and is now known as “the father of venture capital.”

As a public company, ARD was able to attract institutional investors in private equity for the first time. One deal made its reputation: its 1957 investment of $70,000 in equity and approximately $2 million in loans in Digital Equipment Corporation (DEC) provided a substantial return on invested capital after DEC’s initial public offering in 1966. But ARD ultimately ceased to exist for various reasons. It had conflicting goals, as it aimed both at sustaining financial performance and rebuilding the American economy to create jobs for the veterans. Above all, the fact that it was a public company made it impossible to incentivize its managers based on their individual investment decisions. The shareholders / managers misalignment proved fatal: except for DEC, few other investments generated returns for ARD and its shareholders.

Meanwhile, the West Coast was still managing to make it without venture capital. Frederick Terman, who headed the Harvard Radio Research Laboratory during the war, was back on the West Coast as the provost of Stanford University, which he intended to turn into a leading university in the sciences. To achieve that goal, Terman made it a priority to attract the formidable budgets that, following Vannevar Bush’s guidance, the Department of Defense now allocated to advanced research in US universities.

And so it was military procurement, both by the government and weapons manufacturers, that enabled the founding of the first entrepreneurial ventures in what was to become Silicon Valley. The sophisticated system that Terman put in place at Stanford relied on four pillars:

- first, reach out to military prospective customers to better understand their needs, then offer to craft them a prototype in Stanford’s research laboratories—this generated substantial revenue for the university and strengthened its trusted relationship with key military figures;

- second, if the prototype satisfies the customer, encourage one of your students to found a company and manufacture the product at a larger scale—this inspired an entrepreneurial spirit among the students and contributed to stimulating their hard work in the university’s laboratories;

- third, make sure a member of the Stanford faculty (if not Terman himself) becomes a board member or consults with that newly founded company—this contributed to training Stanford scholars in business and turned them into better teachers and researchers;

- fourth, provide office space in the Stanford Technology Park, which was made possible by the fact that the university was the primary land owner in Palo Alto—this ensured that the upstart company stayed close and helped the nascent entrepreneurial ecosystem reach a higher density.

Those strong links, established within a very tight and dense ecosystem, had extraordinary consequences on Stanford. First, it turned it into a financial focal point. Stanford University became the preferred contractor at the prototyping stage, which made Frederick Terman inescapable when it came to gaining access to military budgets: if you wanted to attract defense money for your scientific work, you had to go through Terman. Second, as a result this nascent Stanford ecosystem attracted more promising students, military customers, talented engineers and, later, private investors. Third, it gave rise to a new approach in academic research, driven by the customers’ demands rather than being pushed by laboratories or the agendas of national research agencies. Steve Blank goes as far as to refer to Frederick Terman as the first advocate for the customer development method: while Stanford converted to a customer-driven, entrepreneurial culture, other universities such Berkeley continued their “focus on Big Science and National Lab.” This is what ultimately made Stanford University and Silicon Valley such a magnet for venture capitalists.

At that time, though, there was still no such thing as venture capital in what was known as the Santa Clara Valley. Technology companies were still financed by wealthy individuals, the military-industrial complex or… other technology companies.

Even the first semiconductor companies were not financed by venture capital, but instead by mature companies from the East Coast. Shockley Semiconductor Laboratory was a division of Beckman Instruments, Inc. Fairchild Semiconductor, the legendary firm founded by William Shockley’s “traitorous eight”, was a subsidiary of Fairchild Camera and Instrument. The Fairchild deal was negotiated thanks to Arthur Rock, who was a young New York City investment banker at the time: Rock was so appalled by the difficulties encountered by such a promising tech company that he later went on to found Davis & Rock, one of the pioneering venture capital firms.

Climbing Steps

Venture capital only emerged as an asset class in the 1970s when it came to financing a new industry: personal computing. See our recent issue below to learn more about that historic shift.

Before that there had been a few portentous signals though, with 1957 being the turning point. That year, Tommy Davis (who later founded Davis & Rock with Arthur Rock) invested in Watkins-Johnson on behalf of the Kern County Land Company. A few technology companies went public for the first time, which sent a strong signal that private equity funds could now expect liquidity. In that same period, a few wealthy technology executives started the first angel investment clubs in the Bay Area. Still in 1957, three pioneers founded a new firm called Draper, Gaither & Anderson—but it didn’t last long, as venture capital was only beginning to gain traction.

Then came the Small Business Investment Act of 1958, which was part of a vigorous response (along with the creation of NASA and DARPA) after the Soviet Union’s launch of the Sputnik. The new program led the government to lend money to newly formed investment firms, which were called Small Business Investment Companies (SBIC). It mostly didn’t work, for various reasons described here and here. But it helped younger management teams to start up their businesses and make considerable progress in the methodology for evaluating risks in the technology field — managing SBICs in those years is how legendary venture capitalists like Franklin “Pitch” Johnson learned their business. Finally, all those people looking for the right way to do venture capital settled on the current legal form, limited partnership, and adopted the practice of incentivizing managing partners with a carried interest, finally solving the misalignment problem that had cost General Doriot’s ARD its success.

As it abandoned the SBIC program to craft its own business model, venture capital kept on growing with less paperwork and an improved alignment between limited partners and managing partners. The first management firms emerged to seize that opportunity: Kleiner Perkins Caufield & Byers, the “largest and most established venture capital firm”, was founded in 1972, just one year after the invention of the microprocessor which, according to Carlota Perez, triggered the digital revolution. Sequoia Capital, which was the initiative of yet another legendary investor, Don Valentine, was also founded in 1972.

In 1978 the Department of Labor, following extensive discussions with the newly formed National Venture Capital Association (NVCA), decided to relieve workers’ pension funds from the weight of the old, strict interpretation of the “prudent man rule”. From that date onwards, the largest asset managers were allowed to allocate part of their funds to venture capital. As told by Lionel Pincus, who chaired the NVCA at the time, in the book Done Deals,

On behalf of the NVCA, Charlie Lea and I led the negotiation with the Labor Department of the plan asset rules in 1978 and 1979. That produced the prudent man regulations and the contemporary venture operating company. These regulations made it possible for pension funds to invest directly in venture capital funds, opening a floodgate of new capital for our young industry.

As personal computing reached consumer markets for the first time (notably with the launch of the Apple II), venture capital grew tenfold in the following years. It was fortunate because a new competition was about to storm onto financial markets: leveraged buyouts—which during the 1980s attracted billions when venture capital deals were still counted in the millions. Fortunately, the 1990s tech bubble provided venture capitalists with a new, larger platform on which they could grow up and dance: the Internet. And the rest is history.

Thinking About Venture Capital: The French Case

Reflecting on venture capital is critical. As already explained in a previous issue, it is the means of financing that is most in line with the needs of tech startups at the growth stage.

There have already been radical shifts in the way businesses are financed in a modern economy. The last one was when securities markets took over banks as the number one source of financing (in France, that happened in 1985). Another such shift still must happen to better finance entrepreneurial ventures in the digital economy: venture capital now needs to supersede conservative banking credit as well as short-term securities markets.

The problem is that venture capital still (mostly) works as it did when it was designed in the 1970s, as a relatively marginal asset class. Do we need more of the same old venture capital? Or, as software is eating the world, should we call for a new breed of venture capitalists, more in line with the new challenges that tech companies face in an ever-changing world?

, partner at Kima Ventures (and formerly a partner at The Family), has an unequivocal answer to that question. According to Jean, traditional French venture capitalists got complacent and actually failed on many fronts: bad governance, poor discipline, a passive attitude, a lack of effective software tools, and a constant inability to provide their portfolio companies with relevant, value-adding services.

Others are even crueler than Jean and accuse some French venture capitalists of living off rent. “Did you ever wonder,” an insider once asked me, “why all Paris-based venture capital firms raise a €50M fund?”. The answer is, according to my friend, painfully obvious: with a 2% management fee, three managing partners can typically earn a relatively good wage for nine years, all while enjoying a nice office in the 8th arrondissement of Paris plus the occasional fact-finding trip to Silicon Valley or China.

At the end of the fund, there are two possible outcomes. One is that the performances are “strong” (by a European standard, i.e. the limited partners didn’t lose money). In that case the management team may be able to raise yet another €50M+ fund and keep on living relatively comfortably for another nine years. Or the limited partners lose money, which forces the managing partners to choose another career path after nine years in ventureland. In both cases, it makes sense to question the value that such inept firms add to the startups they invest in. In toxic environments such as Paris, traditional venture capital has in fact become a rent-seeking business: you don’t need strong performances to make a reasonable living and enjoy your power over desperate Entrepreneurs.

But why would limited partners even consider investing in such funds? The answer is… cronyism. In Europe, venture capital weighs so little in the asset allocation strategy of the biggest institutional investors that decisions are not made based on expected returns or any rigorous methodology, but rather because “the managing partner’s been a good friend for 10 years, so why not trust him with those €3M out of the billions I have to allocate?”

A variant is… hype: “Startups are the future: by investing those €5M in that obscure fund, at least I’ll have a story to tell.” But essentially venture capital is so marginal in global asset allocation that your best chance today is to be an insider who plays golf with asset managers and you can then grab the millions needed to fill out your new fund.

The adverse consequences are numerous. Because of the terrible performances, limited partners get used to the idea that venture capital is not significant and should remain a marginal part of asset allocation. And in any case, as pointed out by , top performances are concentrated in a few firms only—a phenomenon that reflects the importance of increasing returns in the digital economy: as winners take most on digital markets, only a few venture capital firms, mostly US-based, are able to reap the rewards. As for the other firms, government agencies such as Bpifrance are here to back them up, but we’re still not sure if it will have the SBIC’s virtuous triggering effect, or if it will maintain the whole system in its current mediocrity.

In places where entrepreneurial ecosystems have taken off, good performances attract more and more capital, to the point where venture capital firms are forced to compete for the better deals, while traditional players, such as Goldman Sachs and Fidelity, are moving into the industry and putting pressure on the incumbents. At the same time, there is an accelerating pace of innovation, particularly at the earlier stages, helped by the rise of innovative firms such as Y Combinator and AngelList. But if venture capital is to rise as an asset class as we wish it to do, radical change has to take over in more toxic environments. If we succeed in the current paradigm shift, future venture capitalists will be very different from today’s venture capitalists, just as traders at today’s Goldman Sachs are different from the old investment bankers of the 1950s.

We founded The Family because we think that the traditional venture capital model is in the course of changing, whether all the players involved are aware of it or not. The imbalance between supply and demand on the global venture capital market has put sleepy venture capital firms in a favorable position: endless lines of Entrepreneurs are waiting and begging for them to invest in their startups. But current trends may be about to take a toll on the traditional model, those small groups of mostly white men reaching consensus on only a few investment decisions every year, while living more or less off management fees after having locked their limited partners in for nine years. We’ll be sharing more on that issue in the coming weeks—stay tuned!

Further Readings

A few readings to go further into the somewhat more complicated history of venture capital:

- Carolyn Tajnai, Fred Terman, The Father of Silicon Valley, Stanford University Press, May 1985.

- Paul A. Gompers, “The Rise and Fall of Venture Capital”, Business and Economic History, 1994.

- The Economist, “The key to industrial capitalism: limited liability”, The Economist, December 1999.

- Lionel Pincus, “The Warburg Pincus Story”, Done Deals: Venture Capitalists Tell Their Stories, Harvard Business Review Press, September 2000.

- Dawn Levy, “Biography revisits Fred Terman’s roles in engineering, Stanford, Silicon Valley”, Stanford Report, November 2004.

- David H. Hsu & Martin Kenney, “Organizing Venture Capital: The Rise and Demise of American Research & Development Corporation, 1946–1973”, Working Paper, 2004.

- , The Secret History of Silicon Valley, 2009.

- Jake Powers, “The History of Private Equity & Venture Capital”, Corporate LiveWire, February 2012.

- , “The Political and Financial Economics of Innovation”, Institute for New Economic Thinking, April 2012.

- Arun Rao and Piero Scaruffi, A History of Silicon Valley, 2013.

- Riva-Melissa Tez (), “Finance: An Industry Based on Psychology”, Medium, November 2014.

- , “The Carlota Perez Framework”, AVC, February 2015.

- , “A Venture Capital History Perspective From Jack Tankersley”, FeldThoughts, August 2015.

(This is an issue of The Family Papers, a series which covers various areas such as entrepreneurship, strategy, finance, and policy. Thanks to , and .)