DECEMBER 2019 QUARTER UPDATE

PERFORMANCE AS AT 31 DECEMBER 2019

| Period |

Fund |

MSCI AC WORLD |

Excess |

| 3 Months |

5.1% |

4.5% |

0.6% |

| 1 Year |

31.7% |

26.8% |

4.9% |

| 2 Years (per annum) |

15.7% |

13.0% |

2.8% |

| Since Inception (per annum)# |

14.2% |

11.9% |

2.3% |

# Inception date 2 June 2017.

Dear Thomas,

The Perpetual Global Innovation Share Fund returned 5.1% net of fees for the December quarter, slightly ahead of the 4.5% return of the MSCI AC World Index. For the 2019 calendar year the Fund returned 31.7%, ahead of the MSCI AC World Index return of 26.8%.

Since the launch of the Fund on the 2nd of June 2017, the Fund has generated a 14.2% per annum return net of fees, ahead of the 11.9% per annum return of the MSCI AC World Index.

The largest contributor this quarter was Axon Enterprise, which benefited from a solid third quarter result driven by strong adoption of the Taser 7 and Axon Body 3. Other contributors included Vestas Wind Systems, Virgin Galactic, Freee, and Alibaba, while Huya, Joyy, Qiwi, and CyberAgent detracted from performance.*

*Companies mentioned above: Axon Enterprise (NASDAQ:AAXN), Vestas Wind Systems (CPH:VWS), Virgin Galactic (NYSE:SPCE), Freee (TYO:4478), Alibaba (NYSE:BABA), Huya (NYSE:HUYA), Joyy (NASDAQ:YY), Qiwi (NASDAQ:QIWI), CyberAgent (TYO:4751).

RENEWABLES

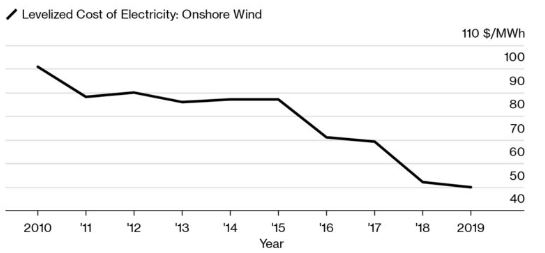

The world is transitioning from fossil fuels to renewables. While this is driven by a desire to tackle climate change, it’s also driven and enabled by the falling cost of renewable energy. We became particularly interested in wind power early last year when we saw that the levelised cost of energy (LCOE) for onshore wind power had become competitive with traditional fossil fuels. Today onshore wind is cheaper than traditional fossil fuels in two-thirds of the world.1 Reaching cost parity is a significant milestone as it transforms the industry from one that’s reliant on government subsidies to one that can thrive on pure economics. If costs continue to fall, which we believe they will, it paves the way for wind power to become a significant portion of the global energy mix.

Cheaper Wind

The cost of wind power has fallen by half since 2010

Source: BloombergNEF

Note: All LCOE calculations are unsubsidised

Offshore wind is an important element of this future energy mix because wind turbines can be built larger, collecting more wind, and there are fewer restrictions on locations. While offshore wind is not yet cost competitive with fossil fuels, it’s expected to reach that point in the next decade (earlier in Europe). A recent report by the International Energy Agency estimates that by 2040 offshore wind will become the largest source of energy in Europe and that global offshore wind capacity will grow by at least 15-fold in the same timeframe.2

We’re also attracted to wind power because it’s an area where bigger is better. The complexity and capital involved in wind means that it’s more likely a smaller number of players will dominate which should lead to better returns than are seen in highly competitive markets with minimal barriers to entry.

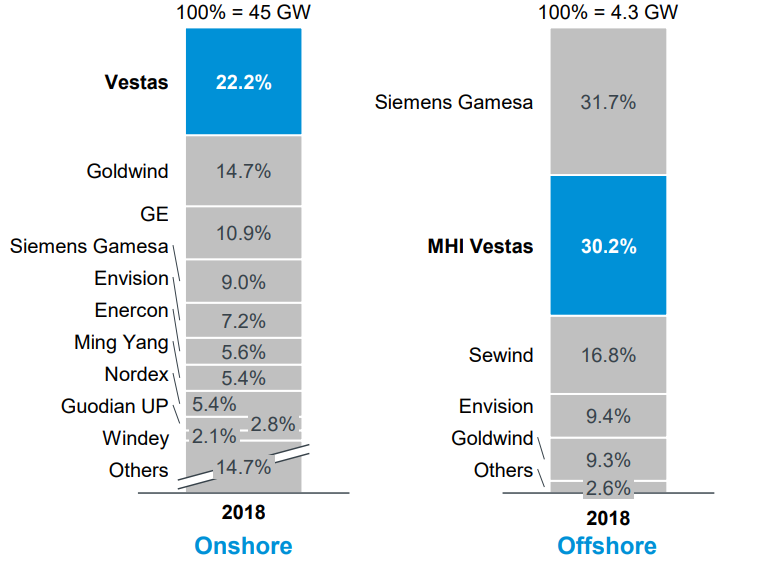

Over the last year we’ve increased our renewables position from zero to 8.6% through investing in two wind-related stocks – RWE, bought in May, and Vestas Wind Systems, bought in August. RWE is a German utilities company that’s in the process of becoming the fourth largest renewables utility in the world and the second largest offshore wind producer in the world. Vestas Wind Systems is the largest onshore wind turbine provider in the world and the second largest offshore wind turbine producer in the world (through a joint venture with Mitsubishi Heavy Industries). Both companies should benefit from growing demand for wind power.

Vestas Wind Systems Market Share

Source: Vestas Wind System

Source: Vestas Wind System

Three of our top five positions at the end of December – Axon Enterprise, Facebook, and SoftBank – became top 5 positions during the quarter.

AXON ENTERPRISE

You may recall that we sold Axon Enterprise back in June 2018.3 We bought back into the stock in February 2019 after it had fallen 17%, and substantially increased our position in October and November as we became more positive on their upcoming Axon Records and Axon Dispatch products.

Axon Records is a records managements system that places video evidence at the heart of the police record. It integrates with Evidence.com, their digital evidence management system, and over time should allow police to reduce duplicate data entry work which will save both time and money. Axon Records is currently being used by two early customers and feedback has been positive.

Axon Dispatch is a police dispatch system that leverages situational features in the Axon Body 3, the new body cameras they started shipping in September. Using Dispatch will allow headquarters to track an officer’s location, any gunshots detected, and if enabled it can transmit live video as well. In critical situations like school shootings and terrorist attacks, this system will give police unprecedented real-time information that can be used to better coordinate officers. Axon Dispatch is expected to start a pilot program this year.

Both products showcase how Axon is leveraging its existing strengths to provide unique, superior products that are difficult for competitors to copy. It also highlights the company’s ability to create new products that improve policing while creating additional value for shareholders.

FACEBOOK

We believe Facebook is cheap and increased our position during the quarter. This is a business that can sustain earnings growth in the mid-to-high teens trading on a forward earnings multiple in the low 20s. It’s difficult to find businesses of comparable quality growing at these rates trading on similar multiples.

We believe the stock is being discounted due to the fear of regulation, which is overstated. Facebook went through the largest privacy regulation in the world, GDPR, in 2018 and came through relatively unscathed. Arguably regulation like GDPR gives a relative advantage to larger businesses like Facebook who can more readily bear the increased cost. If new regulations come in that impact content regulation and censorship, we believe it’s likely to have a similar effect. We think the risk of a breakup is unlikely, but if one were to happen it’s not clear that it would destroy value given we don’t think the market is giving Facebook credit for assets like WhatsApp and Messenger which are currently undermonetised.

SOFTBANK GROUP

We more than doubled our position in SoftBank Group in early November. The stock had fallen 23% from early August due to negative publicity surrounding the failed IPO of WeWork and widespread criticism of SoftBank’s investment in the company (via the SoftBank Vision Fund).

SoftBank Group is an investment company that trades at a 60%+ discount to the value of it's underlying assets. If you assume their investment in the SoftBank Vision Fund (and in WeWork) is worth zero, the company is still trading at a 50%+ discount to the value of its underlying assets. If you include just their three listed investments in their assets – Alibaba, SoftBank KK, and Sprint – and subtract the parent company’s debt, then SoftBank Group is still trading at a 40%+ discount to the value of its underlying assets.

We believe this discount will narrow over time. CEO/Founder Masayoshi Son has committed to not bailing out any other SoftBank Vision Fund companies which should reduce concerns about capital destruction. We also think we’ll see some positive investment stories coming out of SoftBank Vision Fund’s portfolio of 70+ investments over the next year or two. Investments they’ve made in ByteDance, Paytm, Coupang, and Tokopedia all have significant potential.

VIRGIN GALACTIC

“Rutan had a special design for SpaceShipOne, an idea that had come to him in the middle of the night. Essentially, the spaceplane’s wings would be able to detach from the body of the plane and fold upward in what he called a “feather” maneuver. The upright wings would act like the feathers of a badminton shuttlecock, centering the plane by creating drag for a reentry into Earth’s atmosphere so soft that it eliminated the need for a heat shield.”

-- from The Space Barons by Christian Davenport

We bought a small 1% position in space tourism company Virgin Galactic in early December. Normally I wouldn’t write about a 1% position but it’s been a significant contributor to fund performance after rising 47% in December from where we bought it, and a further 48% in January. It’s also the first unprofitable company the fund has invested in since enhancing the fund’s mandate in November.

Virgin Galactic has been on a journey. The original spacecraft, SpaceShipOne, was designed by Burt Rutan in the early 2000s, was funded by Microsoft co-founder Paul Allen, and ended up winning the $10 million Ansari X Prize in 2004 for being the first non-government reusable manned spacecraft to enter space twice within two weeks.

Richard Branson formed Virgin Galactic and acquired the technology in 2004 with the idea that they could use the technology to take passengers to space just three years later. The technology worked, but SpaceShipOne was designed for a single pilot, and they needed a spacecraft designed for a luxury experience that could accommodate two pilots and up to six passengers. This proved to be much more difficult than anticipated, and a tragic accident in 2014 that killed a test pilot further delayed development.

Fast forward to today and the company has made significant progress. It's spacecraft, SpaceShipTwo, has now made two successful test flights to space, and the company is now working on perfecting the passenger experience.

Virgin Galactic went public in October 2019. Rather than doing a traditional IPO they went public via an investment from a SPAC. SPACs are Special Purpose Acquisition Companies that are listed and set up for the specific purpose of investing in a private company, thereby making the private company public. The SPAC originally raised money at $10 per share, and used its cash and equity to merge with Virgin Galactic. The venture capitalist behind the SPAC, Chamath Palihapitiya, invested $100 million of his own money in Virgin Galactic at $10 per share and became the Chairman of the company.

The stock briefly jumped to $11.79 in October post-listing, then drastically fell through November which gave us the opportunity to buy our position in early December at an average price of $7.86. By this stage the company had spent over $1 billion dollars over 15 years to develop its technology, and at that price the value of the company was close to the development cost to date (after adjusting for cash held).

We thought that was a reasonable entry price given the company had passed the point of major technology risks given their two successful flights. While the service hasn’t started yet, we think demand has been proven through strong interest along with the $80 million in cash deposits they collected by 2014 (they stopped pre-sales at that point), and we’re at a point in time where we think the first passenger flights are less than 12 months away.

We think Virgin Galactic has the opportunity to create a high-margin, profitable space tourism business over the next few years which underpins the valuation. We also think they will have no trouble filling demand, and the company will be supply-constrained for at least several years. Longer term there’s considerable optionality around the potential of providing point-to-point suborbital space travel (e.g. San Francisco to Shanghai in 2 hours), which is a capability they’re actively trying to develop over the next 5 to 10 years.

Virgin Galactic’s second flight to space in February 2019

Source: Virgin Galactic on YouTube

After a strong year it’s natural to question whether the market has run its course and is due for a correction. This is not something I spend much time thinking about – at best it’s a distraction as I think it’s very difficult to time the market, and at worst it can keep you from spending the time to find new ideas, and new ideas are the lifeblood of this fund.

The question I focus on is much simpler: Of the roughly 10,000 stocks in the world with a market cap of over A$1 billion, can we find 20 to 60 stocks that we’re happy to own at today’s prices that will provide an attractive return to investors over a 3 to 5 year period?

We believe the answer is yes. The fund ended the quarter owning 37 different stocks – 18 of those we didn’t own at the beginning of the year. Five of the new stocks were positions we’ve held before, like Axon Enterprise, while 13 were brand new to the fund like Vestas Wind Systems and RWE, along with others we haven’t talked about in detail like CD Projekt, Zoom Video Communications, and Merck KGaA.

We’re constantly looking at new and existing ideas, and we actively manage the portfolio so that it always represents what we consider to be the optimal portfolio (with some consideration for reducing adverse tax consequences from over-trading).

I remain excited about what we own today. While we won’t be immune if the market does turn down, I think our current positions will deliver strong returns over a longer multi-year period.

Thank you for your continued support.

|

|

THOMAS RICE

Portfolio Manager

Perpetual Global Innovation Share Fund |

|